Cross-posted from Working America's Main Street blog where I am a featured guest blogger

The Federal Reserve has justifiably faced serious criticism for its failure to control the $8 trillion housing bubble and its subsequent bursting, with the combination of economic devastation and financial crisis that ensued. In response to the onslaught of the Great Recession, the Fed has kept short-term interest rates near zero, extended extraordinary amounts of money to the largest banks, and supported monetary policies that at least have not impeded the positive, stabilizing effects of federal stimulus efforts.

But that's been about it.

We still face an outrageous unemployment crisis, an economy burdened by depressed demand and, except for corporate profits, an anemic private sector when it comes to business investment and job growth.

We still face an outrageous unemployment crisis, an economy burdened by depressed demand and, except for corporate profits, an anemic private sector when it comes to business investment and job growth.

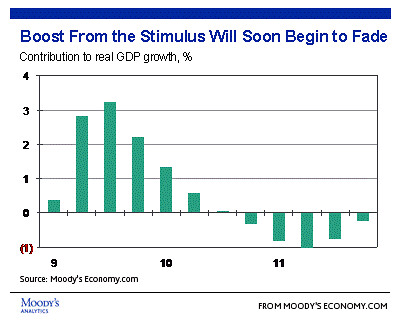

Now, however, with the expected impact on growth of the stimulus program waning, and the administration and the Congress all but hamstrung by a ruling Republican minority in the Senate, a growing number of economists are warning of the danger of a double-dip recession, or deflation, or both. And they are calling on the Fed, which has certainly done plenty to bolster Wall Street, to use all of its tools and do more to help Main Street.

Not surprisingly, Paul Krugman, the Nobel Laureate economist and New York Times columnist, has been vociferous and unabashed in his repeated calls for more effective Fed actions to address both high unemployment and deflationary dangers.

The Federal Reserve's legislated mandate is "to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates."

Well, with nearly 15 million workers unemployed, and almost half for six months or more, it's pretty obvious that the Fed isn't doing its job on the employment front. But, as Krugman noted recently, the Fed is also "consistently missing its inflation target." He is urging the Fed to both raise its target inflation rate -- to encourage spending and investment -- and to buy additional assets, particularly long-term Treasury securities.

Economist Dean Baker has been urging similar action as well. Specifically, Baker is urging the Fed to buy and hold long-term Treasury debt:

There is a simple way to avoid a sharp rise in the interest burden associated with a higher debt. The Federal Reserve Board can buy and hold the debt that is currently being issued by the Treasury to finance the deficit. The logic of this is straightforward. If the Fed holds the debt, then the interest on the debt is paid to the Fed. The Fed then returns the interest to the Treasury each year, meaning the net cost to the government is zero.

This is not slight of hand. The point is that the economy has a huge amount of idle resources in the form of unemployed workers and excess capacity. In this situation, the increased demand created by government spending does not have to come at the expense of existing demand. The economy can simply expand to fill the additional demand created by larger deficits. While that may not be true in five or ten years, assuming the economy is again near full employment, right now deficits need not lead to either higher interest rates or higher inflation.

In fact, the financial markets and the "bond market vigilantes" should even support the decision to have the Fed purchase and hold the government debt being issued now to finance the deficit. This practice will lessen the future interest burden on the Treasury.

In an article in the recent issue of The Nation, Baker also explains that:

The roots of this economic crisis are very much centered in the growth in inequality over the past three decades. This becomes clear once we recognize that the financial turmoil is a minor aspect of the overall crisis, and that its primary cause is the economic imbalances created by the housing bubble.

Baker describes how the growing economic inequality in the U.S., with the wealthiest taking an ever-increasing share of incomes at the expense of both middle-class and lower-income workers, itself fostered the growth of a series of asset bubbles, which in turn exacerbated the inequality.

So, in addition to aggressively pursuing additional stimulus, the Fed should move to rein in CEO compensation and bankers' bonuses while supporting a modest financial speculation tax.

The chances for any of these remedies to be taken up by the Fed have been slim, at best, until now. Granted, there are a some at the Fed who, like European Central Bank president Jean-Claude Trichet, remain in the grip of the Contraction = Expansion delusion, and are chomping at the bit to raise interest rates to fight a non-existent inflation. But, fortunately, they are a minority.

As Sewell Chan reported in a New York Times story headlined Fed Leaders Show Division Over Deflation:

The Federal Reserve disclosed on Wednesday that its chief policy makers were divided on whether the weak economy faced a new, potentially dangerous threat in the form of deflation.

[...]

With Congress deadlocked over fiscal policy, attention has shifted to monetary policy as a tool for attacking the 9.5 percent unemployment rate. But on that score, the Fed is also divided, though its disagreements are expressed in a far more genteel manner.

On Wednesday, the Fed lowered its estimate of economic growth for this year, to a range of 3 to 3.5 percent, from the 3.2 percent to 3.7 percent forecast in April. Inflation has been running well below the Fed’s unofficial target of nearly 2 percent, so much so that a few officials fear that the United States is at risk of the kind of deflationary spiral that has hobbled the Japanese economy for the better part of two decades.

The article then quotes from the just-released minutes of the Fed's Open Market Committee's June meeting:

"Several participants noted that a continuation of lower-than-expected inflation and high unemployment could eventually lead to a downward movement in inflation expectations that would reinforce disinflationary pressure," the minutes stated. "By contrast, a few participants noted the possibility that a potentially unsustainable fiscal position and the size of the Federal Reserve’s balance sheet could boost inflation expectations and actual inflation over time." (emphasis added - MH)

I would imagine that, even at the Fed, several is more than a few.

And if a few more could be added to the current several, perhaps that would result in lots of support for the kinds of vigorous Fed actions advocated by Krugman and Baker.

That's not quite what I'd call likely, but it's at least much more feasible now, with the Senate taking up the nominations of three new Obama administration picks to fill vacancies on the Fed's Board of Governors -- and the cause of aggressive Fed action being given a clear boost by Banking Committee Chairman, Sen. Chris Dodd (D-CT):

Is a key senator trying to encourage the Fed to pursue a looser monetary policy? In his opening statement at a confirmation hearing for three nominees to be Federal Reserve Board governors, Sen. Christopher Dodd (D-Conn.) came pretty darn close to calling for the central bank to take new steps to support growth.

"While the economy is growing, it is not growing fast enough to help the millions of Americans who lost their jobs as the result of the crisis," said Dodd, chairman of the Senate Banking Committee. He noted that the unemployment rate remains very high, business investment is subdued and that some price measures "suggest that we are moving toward price deflation."

"It is evident that the economy is going to need all the help the Fed can provide over the coming year," he said.

Dodd's comments came at the opening of a committee hearing with the new Federal Reserve Board nominees -- San Francisco Fed president Janet Yellen, MIT economist Peter Diamond, and Maryland's commissioner of financial regulation Sarah Bloom Raskin.

The Wall Street Journal reported:

Ms. Yellen and Ms. Raskin both acknowledged the importance of stable prices—half the Fed's mandate—but they stressed the importance of boosting the economy.

"Over the next few years, the Fed must craft policies that ensure that our economy accelerates its progress along the recovery path it has begun to trace," Ms. Yellen said. "With unemployment still painfully high, job creation must be a high priority of monetary policy."

While the Fed achieved price stability for a generation, Ms. Raskin said, "it is only a partial victory when many American households continue to face the perils of unemployment and many small businesses struggle with weakened consumer demand and reduced access to credit."

The Washington Post reported that Ms. Yellen also stated that considering "further fiscal stimulus now... is natural given the outlook" for slower growth than was projected only a few months ago.

Raskin, the Maryland commissioner for financial regulation, explicitly stresses the need for the Fed to combat unemployment.

"We need to strengthen this recovery by expanding its foundations. This means that, in addition to maintaining stable inflationary expectations and keeping a vigilant eye on the emergence of new bubbles, the Fed must seek to fulfill the other part of its statutory mandate by addressing unemployment, which has pervasive social costs."

The three Fed nominations require Senate confirmation. In its report, Reuters quoted Senator Dodd as saying:

"My guess is we probably won't get to them until probably September," Dodd told reporters.

Waiting for the Senate. Do I need to ask why that sounds so infuriatingly repetitive? Meanwhile, as Paul Krugman says:

But here we are, visibly sliding toward deflation — and the Fed is standing pat.

What should it be doing? Conventional monetary policy, in which the Fed drives down short-term interest rates by buying short-term U.S. government debt, has reached its limit: those short-term rates are already near zero, and can’t go significantly lower. (Investors won’t buy bonds that yield negative interest, since they can always hoard cash instead.) But the message of Mr. Bernanke’s 2002 speech was that there are other things the Fed can do. It can buy longer-term government debt. It can buy private-sector debt. It can try to move expectations by announcing that it will keep short-term rates low for a long time. It can raise its long-run inflation target, to help convince the private sector that borrowing is a good idea and hoarding cash a mistake.

Nobody knows how well any one of these actions would work. The point, however, is that there are things the Fed could and should be doing, but isn’t.